If you’re paying $100 or more each month for a prescription, you’re not alone. Millions of people on Medicare Part D and other private insurance plans face high copays for medications that aren’t on the lowest cost tier. But here’s the thing: tier exceptions can cut those costs by 50%, 80%, or even 100%-if you know how to ask for them.

A tier exception isn’t a loophole. It’s a formal request your doctor can make to your insurance plan to move a drug from a high-cost tier to a lower one. For example, if your medication is on Tier 3 (say, $50 per month) but should be on Tier 1 ($0-$15), you could save $35-$50 every time you refill. That’s $420-$600 a year, just by filling out a form.

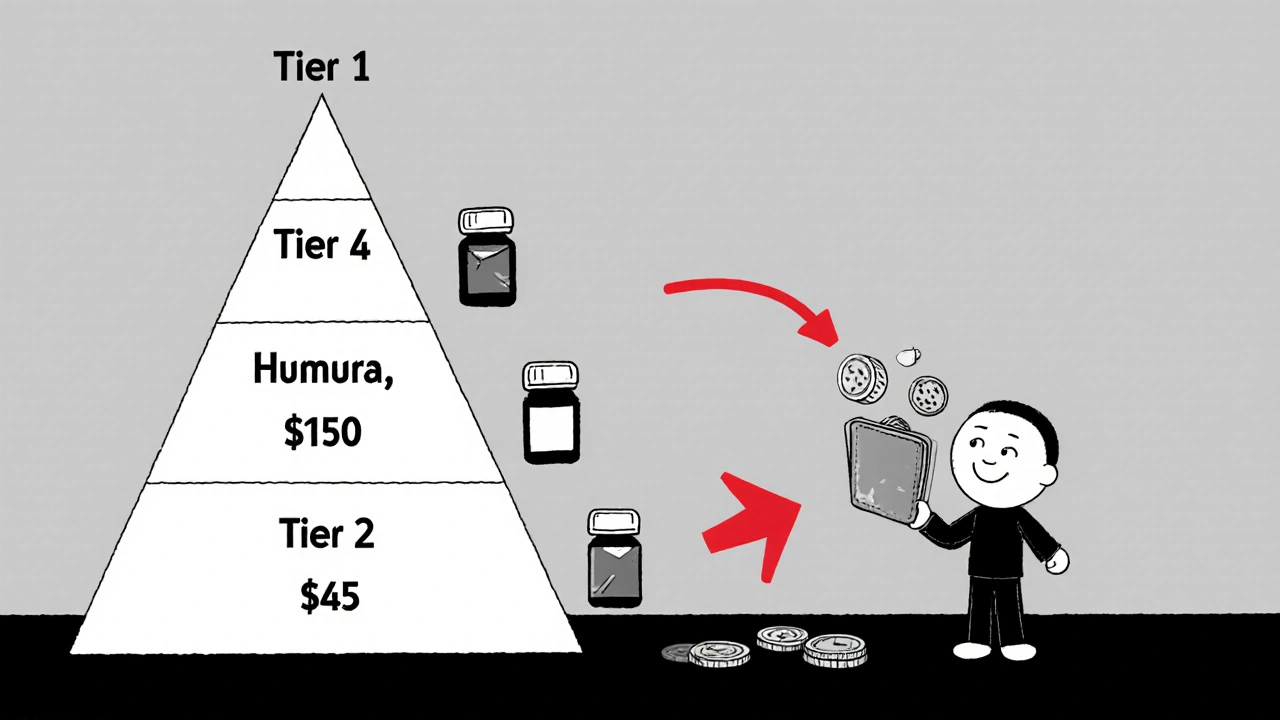

How Drug Tiers Work

Most insurance plans, including Medicare Part D, group medications into tiers based on cost. The lower the tier, the less you pay. Here’s how it typically breaks down:

- Tier 1: Generic drugs. Copay: $0-$15

- Tier 2: Preferred brand-name drugs. Copay: $15-$40

- Tier 3: Non-preferred brand-name drugs. Copay: $40-$100

- Tier 4: Preferred specialty drugs. Coinsurance: 20-30%

- Tier 5: Non-preferred specialty drugs. Coinsurance: 30-40% or more

It’s not about which drug is better for your health-it’s about which ones your insurer negotiated a better price for. A drug might be the most effective treatment for your condition, but if it’s not on the preferred list, you pay more.

For example, Humira (a biologic for rheumatoid arthritis) often lands on Tier 4 or 5. Without a tier exception, you could pay $150 a month. With one, it could drop to $45-or even $0-if moved to Tier 1.

When a Tier Exception Makes Sense

You don’t need a special reason to ask for a tier exception. You just need a reason your current drug works better for you than the lower-tier alternatives. Here are common situations where tier exceptions succeed:

- You had bad side effects from the preferred drug (like nausea, dizziness, or skin reactions)

- The preferred drug didn’t work at all for your condition

- You’re stable on your current drug and switching would risk your health

- You have a chronic condition like multiple sclerosis, Crohn’s disease, or heart failure where specific medications are proven to be more effective

According to the Medicare Rights Center, 58% of people who request tier exceptions get them approved. The biggest reason people fail? Not giving enough medical detail.

How to Request a Tier Exception

There are three steps-and only one of them needs you to do anything.

- Ask your doctor to submit the request. You can’t file this yourself without their signature and clinical notes. Call their office and say: “I need a tier exception for my medication. Can you help me file one?”

- Your doctor fills out the form. Most insurers have a standard form. Some allow electronic submission through their portal. The key part? The clinical justification. Your doctor must explain why lower-tier alternatives won’t work for you. Generic statements like “I don’t like the other drug” won’t cut it. They need specifics: “Patient developed GI bleeding on warfarin, requiring a switch to apixaban due to increased bleeding risk with anticoagulants.”

- Submit and wait. Your doctor’s office usually handles submission. If you’re unsure, ask them to confirm it was sent. Plans must respond within 72 hours if your doctor says your health is at risk, or within 14 days for a standard request.

Pro tip: Request the exception before you fill your first prescription. If you’ve already paid full price, you might still get a refund for past fills-some plans allow retroactive adjustments.

What Makes a Tier Exception Approved

Approval rates jump from 31% to 72% when the request includes strong clinical documentation. Here’s what works:

- Use exact medical terms. “Patient has uncontrolled atrial fibrillation” is better than “heart issues.”

- Reference past failures. “Patient tried lisinopril and experienced persistent cough and angioedema.”

- Include lab results or hospitalizations. “Hospitalized in March 2025 for acute kidney injury after starting generic furosemide.”

- Don’t say “I prefer.” Say “This drug is medically necessary.”

Insurers approve 62% of requests with complete documentation. But 37% of initial denials happen because the doctor’s note is too vague. If you get denied, don’t give up. You can appeal. And 78% of appeals with better documentation get approved.

Real Stories, Real Savings

One Reddit user, “PharmaPatient87,” shared that their doctor submitted a tier exception for Humira. It moved from Tier 4 ($150/month) to Tier 3 ($45/month). Approval took 10 days. That’s $1,260 saved in a year.

Another user tried twice for Xarelto. The first time, the doctor’s note said “patient has difficulty with blood thinners.” Denied. The second time, they wrote: “Patient experienced recurrent epistaxis and hematuria on rivaroxaban, requiring switch to apixaban due to lower bleeding risk in elderly patients.” Approved-moved to Tier 2, copay dropped from $60 to $40.

According to a 2023 survey of 1,200 Medicare beneficiaries, the average savings per approved tier exception was $37.50 per fill. Multiply that by 12 fills a year, and that’s $450 saved-just for one drug.

What to Do If It’s Denied

Denial doesn’t mean no. It means “try again with better info.”

- Get a copy of the denial letter. It should say why.

- Ask your doctor to write a stronger letter. Include specific side effects, lab results, or treatment history.

- Call your insurance plan and ask for the appeals process. Most have a 60-day window.

- If you’re overwhelmed, contact the Medicare Rights Center or your State Health Insurance Assistance Program (SHIP). They offer free help.

Some plans even let you request an external review if your appeal is denied. That means an independent doctor reviews your case.

Timing Matters

Don’t wait until your prescription runs out. The best time to request a tier exception is right after your doctor writes the prescription. That’s called a “proactive tier exception.”

According to the Medicare Rights Center, proactive requests have an 89% same-day approval rate. Reactive requests-those made after you’ve paid full price-only get approved 67% of the time.

Some insurers, like UnitedHealthcare, now offer pre-approval tools that let doctors check if a drug is likely to be approved before they even submit. That cuts approval time from 9 days to under 4 days.

What’s Changing in 2025

The Inflation Reduction Act caps out-of-pocket drug costs at $2,000 a year for Medicare beneficiaries starting in 2025. That’s huge. But here’s the catch: that cap only kicks in after you’ve spent $2,000. If you’re paying $100 a month for a drug, you’ll hit that cap in 20 months. But if you lower that copay to $45, you’ll only spend $540 a year-and never hit the cap at all.

Tier exceptions still matter. Even with the cap, they reduce your spending during the initial coverage phase, help you avoid the coverage gap (donut hole), and lower your overall out-of-pocket burden.

Specialty drugs-like those for MS, RA, or cancer-are driving most tier exception requests. They make up just 2% of prescriptions but 53% of total drug spending. If you’re on one of these, a tier exception isn’t just helpful-it’s essential.

Bottom Line

Tier exceptions are the most underused tool for lowering prescription costs. Only 18% of eligible patients try for one-even though they can save hundreds or thousands per year.

You don’t need to be a medical expert. You just need to ask your doctor to help you file one. Make sure they explain why your drug is necessary, not just that you want it. Submit early. Appeal if denied. And don’t assume your copay is fixed.

That $100-a-month drug? It might cost you $0. You’ll never know unless you ask.

What is a tier exception for medication?

A tier exception is a formal request to your insurance plan to move a medication from a higher-cost tier to a lower one on the formulary. This lowers your copay. It’s not for drugs not on the formulary-that’s a formulary exception. A tier exception applies when the drug is covered but priced at a higher cost-sharing level than medically necessary.

Who can request a tier exception?

You, your doctor, or your authorized representative can start the request. But only your doctor can provide the medical justification required. Insurance plans require a written statement from your prescriber explaining why lower-tier alternatives won’t work for you due to efficacy, safety, or side effects.

How long does a tier exception take to get approved?

For standard requests, plans have up to 14 days to respond. If your doctor says your health could be harmed by a delay, it’s an expedited request-and they must respond within 72 hours. Proactive requests (submitted before filling the prescription) often get approved the same day, especially with newer insurer tools.

Can I get a tier exception for any drug?

Only if the drug is already on your plan’s formulary. If it’s not covered at all, you need a formulary exception instead. Tier exceptions are for drugs that are covered but placed on a higher tier. Common candidates include biologics for rheumatoid arthritis, specialty drugs for multiple sclerosis, and certain heart or kidney medications.

What if my tier exception is denied?

You can appeal. Most denials happen because the clinical documentation is too weak. Ask your doctor to rewrite the letter with specific medical details-side effects, failed trials, lab results, or hospitalizations. Then submit an appeal within 60 days. About 78% of appeals with better documentation get approved.

Do tier exceptions work for private insurance, not just Medicare?

Yes. While Medicare Part D has the most public data, most private insurers (like UnitedHealthcare, Aetna, Cigna) use tiered formularies and offer tier exceptions. The process is similar: doctor’s note, form submission, and clinical justification. Check your plan’s website or call customer service to ask about their tier exception policy.

Will a tier exception affect my coverage gap (donut hole)?

Yes-potentially in a good way. If your drug is moved to a lower tier, your out-of-pocket costs drop, which means you reach the coverage gap later-or may not reach it at all. Lower copays also reduce the total amount you spend in the initial coverage phase, helping you qualify for catastrophic coverage faster.

Can I get a tier exception for over-the-counter drugs?

No. Tier exceptions only apply to prescription drugs covered under your plan’s formulary. Over-the-counter medications are not included in tiered structures and are rarely covered by insurance unless prescribed and submitted under special circumstances (like insulin under certain plans).

How often can I request a tier exception?

You can request a tier exception anytime you’re prescribed a new medication or if your current drug’s tier changes. If your drug’s copay increases mid-year due to a plan update, you can file a new request. There’s no limit, as long as you have a valid medical reason.

Do I need to pay for the drug while waiting for approval?

You can choose to pay the full price while waiting. But if your request is approved, many plans will refund the difference for fills during the review period. Some pharmacies can even hold your prescription until approval. Ask your pharmacist or insurance plan about their policy on retroactive adjustments.

Kelsey Worth

November 28, 2025 AT 05:07Nirmal Jaysval

November 28, 2025 AT 13:26Emily Rose

November 29, 2025 AT 17:27Benedict Dy

November 30, 2025 AT 02:29Emily Nesbit

December 1, 2025 AT 11:01John Power

December 1, 2025 AT 18:57Richard Elias

December 2, 2025 AT 15:30Scott McKenzie

December 3, 2025 AT 05:47Jeremy Mattocks

December 4, 2025 AT 10:59Paul Baker

December 6, 2025 AT 00:00Zack Harmon

December 6, 2025 AT 02:12Jeremy S.

December 7, 2025 AT 04:45Jill Ann Hays

December 7, 2025 AT 19:47Sarah McCabe

December 8, 2025 AT 02:59