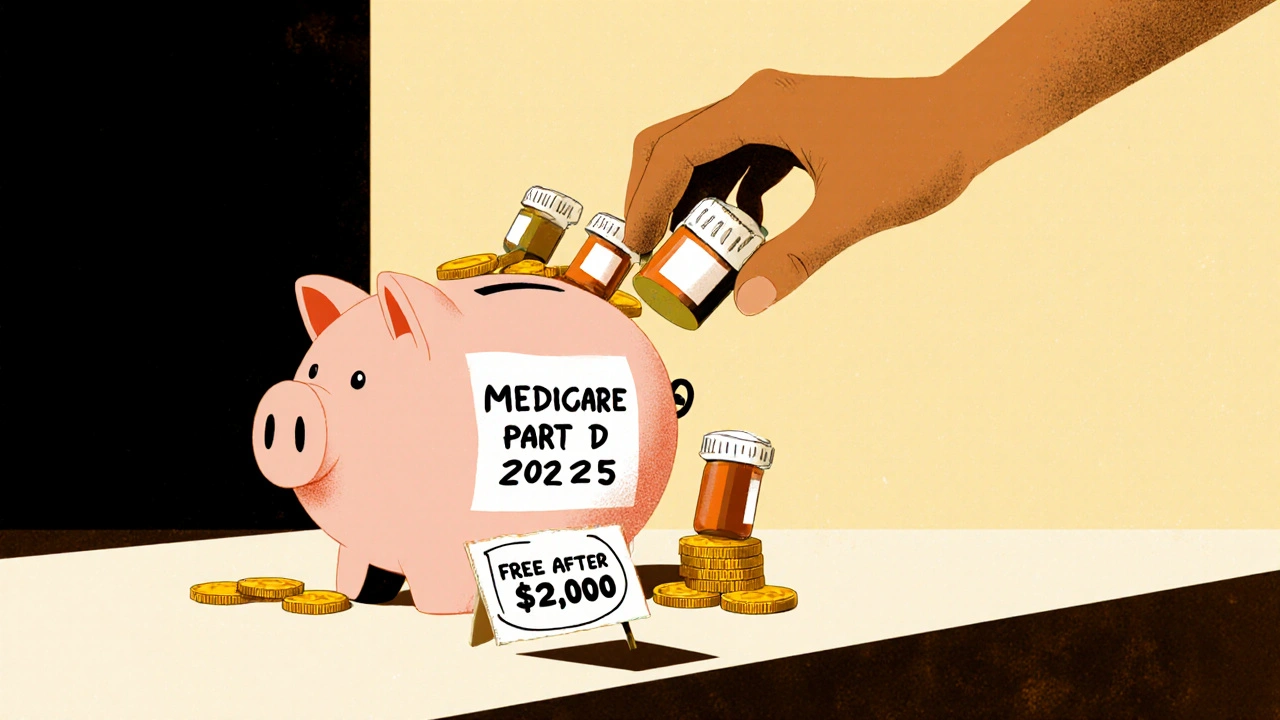

By 2025, if you're on Medicare and take generic medications, your out-of-pocket drug costs could drop by hundreds of dollars a year-maybe even to $0. That’s not a guess. It’s the new reality thanks to changes from the Inflation Reduction Act. The big shift? A hard cap on what you pay for prescriptions each year: $2,000. Once you hit that number, your generic drugs cost nothing for the rest of the year. No more surprise bills. No more choosing between meds and groceries.

What Changed in Medicare Part D in 2025?

Before 2025, Medicare Part D beneficiaries had to spend nearly $8,000 out of pocket before reaching catastrophic coverage. That meant someone taking a few generic pills every day could be stuck paying hundreds of dollars a month for years. Now, that ceiling is gone. The $2,000 cap applies to everyone, no matter how many prescriptions they take. And it includes everything you pay: deductibles, copays, coinsurance. Even manufacturer discounts count toward it.That’s huge for people on chronic meds-like blood pressure, diabetes, or cholesterol drugs. Most of these are generics. In 2024, 84% of all Part D prescriptions were generics, but they made up only 27% of total spending. Why? Because they’re cheap. And now, the system is built to reward that.

How Much Do Generics Actually Cost Now?

In 2025, the average copay for a 30-day supply of a preferred generic drug is about $10. That’s the same whether you’re in a stand-alone Part D plan or a Medicare Advantage plan with drug coverage. For many people, that’s less than what they pay for coffee each week.But here’s the catch: not everyone gets to skip the deductible. About 85% of stand-alone Part D plans still have one-up to $590 in 2025. That means if you take a $10 generic, you pay the full $10 until you meet that deductible. After that, you pay 25% coinsurance until you hit the $2,000 cap. Then? Free. No more payments. No more limits.

For low-income beneficiaries, it’s even better. If you qualify for Extra Help (Low-Income Subsidy), your deductible is $0, and your generic copays are between $0 and $4.50. That’s less than the cost of a bus ticket.

Part D Plans vs. Medicare Advantage: Which Saves More?

It’s easy to assume Medicare Advantage (MA-PD) plans are better because they bundle medical and drug coverage. And for most people, they are. The average monthly premium for drug coverage in an MA-PD plan is just $7. Compare that to stand-alone Part D plans, which average $39 a month. That’s over five times more.But here’s what most people don’t realize: your copays for generics are nearly identical between the two. So if you’re only taking generics, the real savings come from lower premiums and the $2,000 cap. MA-PD plans often include extra benefits-like dental or vision-and sometimes lower premiums. But stand-alone plans might have better formularies for specific drugs. That’s why you need to check your exact meds.

Why Some People Still Pay More Than Expected

The system is simpler now, but it’s not foolproof. A lot of people get tripped up by how the $2,000 cap is calculated. Only what you pay out of pocket counts-premiums don’t. And not all discounts count the same. Manufacturer coupons? Those don’t count toward the cap. But the discounts drugmakers are now required to give under the Inflation Reduction Act? Those do.Another issue: therapeutic substitution. Some plans swap one generic for another-even if they’re chemically identical-because the new version has a lower copay. You might end up with a different pill shape or brand name, and your doctor didn’t sign off on it. That’s legal, but it’s confusing. In 2024, Medicare’s helpline saw a 23% jump in calls about this.

And then there’s the formulary. Not all plans cover every generic. Some require step therapy-meaning you have to try a cheaper generic first before they’ll approve a slightly more expensive one. About 27% of plans use this for at least 15 drug classes. If you’ve been on the same med for years, you might get a surprise letter saying your drug is no longer covered unless you try something else.

Who’s Saving the Most?

The biggest winners are people taking multiple generics-especially those who hit the $2,000 cap. The Centers for Medicare & Medicaid Services estimates that in 2025, Part D beneficiaries will save a total of $7.4 billion collectively. That’s an average of $400 per person who takes generics.One Reddit user, a retired pharmacist, wrote: “My generic blood pressure meds now cost me $0 after hitting the $2,000 cap. Last year, I paid $1,200 more for the same drugs.” That’s not rare. It’s becoming normal.

But not everyone feels it yet. A CMS survey found that only 68% of generic users are satisfied with their coverage-compared to 79% of brand-name users. Why? Because brand-name users often get direct discounts from manufacturers, which don’t count toward the cap. Generics don’t have those. So if you’re on a brand, you might see a lower bill, but your out-of-pocket spending doesn’t count toward the cap. It’s a quirk in the system.

How to Make Sure You’re Getting the Best Deal

You don’t have to guess. Use the Medicare Plan Finder tool. It’s updated every October. Type in your exact medications-name, dose, how often you take them-and it will show you which plans charge the least for your generics. It also shows you if you’ll hit the $2,000 cap early, and when your drugs will become free.But here’s the problem: 32% of people who use the tool need help navigating it. That’s why calling 1-800-MEDICARE or asking a local State Health Insurance Assistance Program (SHIP) counselor can save you hundreds. They’ll walk you through formularies, copays, and what counts toward the cap.

Don’t assume your plan from last year is still the best. Plans change their formularies every year. A drug that was cheap in 2024 might be tier 3 in 2025. And if you’re on Extra Help, you can switch plans anytime-no waiting for Open Enrollment.

What’s Coming Next?

In 2026, a new program called the Selected Drug Subsidy Program will kick in. It gives Part D plans a 10% subsidy if they lower copays for certain high-cost generics. That could mean even lower prices for drugs like insulin or certain heart medications-even if they’re technically generics.Biosimilars are also coming fast. These are like generic versions of complex biologic drugs-think cancer or autoimmune meds. By 2028, they could make up 35% of that market. That’s another wave of savings on the horizon.

But there’s a warning: some plans may start restricting access to high-cost generics to avoid losing money. That’s because under the new rules, plans now pay more of the cost after you hit the cap. So they might push you toward cheaper alternatives-even if they’re not better.

Bottom Line: Generics Are Your Best Friend

If you’re on Medicare and take generic drugs, you’re living through the biggest shift in prescription drug pricing in decades. The $2,000 cap is real. The savings are real. And for many, it means finally being able to afford the meds they need without fear.Check your plan every year. Use the Plan Finder. Ask for help if you’re confused. And remember: once you hit that $2,000 cap, your generics are free. No more bills. No more stress. Just your pills-and your peace of mind.

steffi walsh

November 17, 2025 AT 12:53Finally! I’ve been skipping my blood pressure pills for years because of the cost. This year, I filled my script and cried in the pharmacy. No joke. $0. Just… $0. I’m not even mad anymore. Just tired of being scared.

Shaun Barratt

November 19, 2025 AT 01:37It’s worth noting that the $2,000 out-of-pocket cap applies only to beneficiary payments-not premiums, not manufacturer coupons, and not non-covered drugs. Many beneficiaries misunderstand this, assuming their entire drug spending is capped. The CMS data shows a 38% error rate in self-reported cap awareness. Always verify with the Plan Finder.

Iska Ede

November 20, 2025 AT 09:53So let me get this straight-my $12 insulin is free now, but my $150 brand-name antidepressant still costs me $80 because it doesn’t ‘count’? Thanks, capitalism. At least my coffee’s still cheap.

Christine Eslinger

November 21, 2025 AT 04:50This change is the most humane thing Medicare’s done in 20 years. I used to watch my mom ration her metformin-half a pill every other day. Last month, she told me she’s taking her full dose again. Said she finally feels like a person, not a cost center. That’s not policy. That’s dignity.

And yes, the formulary swaps are wild. My dad got switched from lisinopril to enalapril because the plan got a better deal. Same active ingredient. Different pill shape. Different color. Different panic attack. He called his doctor in tears. The system needs better communication, not just savings.

Also, Extra Help is underused. If you’re on SSDI or make under $20k/year, you qualify. Even if you think you don’t. Call 1-800-MEDICARE. They’ll walk you through it. No judgment. No forms. Just help.

And if you’re on Medicare Advantage, check your pharmacy network. Some plans have one pharmacy in your whole county. One. That’s not access. That’s a trap.

Denny Sucipto

November 23, 2025 AT 01:33I’ve been a pharmacy tech for 17 years. I’ve seen people cry because they couldn’t afford their meds. I’ve seen them choose between insulin and groceries. I’ve seen them swallow half a pill and say ‘it’s fine.’

This $2,000 cap? It’s not magic. It’s justice. Slow justice. But justice.

My aunt hit the cap in March. She started buying groceries again. Bought a new pair of shoes. Said she felt like she could breathe. That’s what this is. Not savings. Survival.

Conor McNamara

November 24, 2025 AT 20:59they say its free now but i think the gov is just hiding the cost somewhere else… like maybe theyre raising taxes or something… i heard the drug companies are just raising prices on the non-generic stuff to make up for it… its all a scam… i saw a video on youtube about this…

Leilani O'Neill

November 26, 2025 AT 14:38Let’s be honest-this only benefits the lazy. People who don’t bother to research their options or shop around. Why are we subsidizing poor financial planning? If you can’t manage your own health expenses, maybe you shouldn’t be on Medicare at all. This is just another entitlement snowball.

Riohlo (Or Rio) Marie

November 28, 2025 AT 08:05How quaint. The proletariat now gets to pay $10 for lisinopril. How noble. Meanwhile, the real pharmaceutical innovation-the biosimilars, the GLP-1 agonists, the targeted cancer therapies-are being strangled by this populist cap. The system isn’t saving people. It’s punishing innovation. And you, my dear, are the beneficiary of a dying paradigm.

Brenda Kuter

November 28, 2025 AT 21:05MY NEIGHBOR’S SON GOT HIS INSULIN FOR $0 AND NOW HE’S NOT TAKING HIS OTHER MEDS BECAUSE HE THINKS IT’S ALL FREE. I SAW IT WITH MY OWN EYES. HE THOUGHT THE $2000 CAP MEANT EVERYTHING WAS FREE. THIS IS A DISASTER. THEY NEED TO TEACH PEOPLE HOW THIS WORKS OR PEOPLE WILL DIE.

Gabriella Jayne Bosticco

November 30, 2025 AT 08:45One thing no one talks about: the mental load. For years, we were terrified of running out of meds. Now, for the first time, I can sleep. Not because I’m rich. Because I’m not afraid anymore. That’s not a policy win. That’s a soul win.

And yes, the formulary swaps are confusing. But if you call your SHIP counselor, they’ll explain it in plain English. No jargon. No pressure. Just help. You’re not alone.

Sarah Frey

November 30, 2025 AT 15:58The $2,000 cap is a structural reform, not a temporary fix. It aligns incentives: plans now benefit from keeping people healthy, not just collecting premiums. That’s a paradigm shift. But implementation remains uneven. Many beneficiaries still don’t know how to use the Plan Finder. Community outreach is critical.

Also, therapeutic substitution is legal but ethically fraught. Clinicians should be consulted before switching generics, even if they’re bioequivalent. Patient autonomy matters.

Holly Powell

November 30, 2025 AT 17:35The real issue isn’t the cap-it’s the formulary design. Tiered structures incentivize plans to push lower-cost generics even when they’re suboptimal. The $2,000 cap merely masks the underlying perverse incentives. We need mandatory formulary transparency, not just cost caps. Otherwise, we’re just rearranging deck chairs on the Titanic.

Shilpi Tiwari

December 1, 2025 AT 07:12From a pharmacoeconomic standpoint, the Inflation Reduction Act’s restructuring of Part D represents a significant shift in risk allocation from beneficiary to plan sponsor. The $2,000 OOP cap, coupled with mandatory manufacturer discounts, effectively transfers $7.4B in cost burden-per CMS projections-onto the payer side. However, this creates moral hazard: beneficiaries may overutilize low-cost generics, potentially increasing utilization rates beyond actuarial assumptions. The long-term fiscal sustainability hinges on whether plan sponsors can negotiate adequate rebates to offset increased utilization.

Hal Nicholas

December 2, 2025 AT 14:16Everyone’s acting like this is a miracle. But what about the people who take brand-name drugs? They’re getting screwed. The system rewards generics, but what if your body doesn’t respond to the generic version? You’re stuck paying full price while others get free meds. That’s not fair. That’s discrimination.

Louie Amour

December 4, 2025 AT 12:14Oh, so now we’re rewarding people for taking cheap pills? What’s next? A prize for not smoking? A medal for brushing your teeth? This isn’t healthcare reform. It’s moral superiority theater. People should be responsible for their own health choices, not handed freebies because they didn’t plan ahead.